1. The twenty+ point Blufountain African Insurance Digital Transformation Guidelines.

1.1 Background:

The Blufountain insurance guidelines were designed for emerging African insurers to transform into modern insurers. Key among the 20 points of recommendation and guidelines is to measure the success of that insurer as it transforms into the future. The Blufountain Digital Transformation guidelines do work with other major blueprints in insurance and one can assess their insurer for readiness using the same guidelines.

Recommendations however will differ country to country based on regulatory limitations and economy size.

1.2 What is digital transformation in insurance?

Digital transformation in banking refers to integrating various fintech technologies to automate, optimize, and digitize processes in the banking industry.

1.3 How mature is Digital transformation in African insurance?

African insurers suffer from digital challenges like data costs, network challenges , regulatory frameworks , skills migration to Europe slow government technological advancements, currency fluctuations, and high unemployment in some key African countries.

The insurance industry is embracing transformation to keep pace with the ongoing digital disruption across global markets and economies. A combination of factors – including changing consumer demography, new demand patterns, new market entrants, profitability concerns, and operational resilience – are urging this dramatic shift.

1.4 How can the African insurers transform into a modern insurers?

For African insurers with huge young population growth , massive urbanization with cities like Dar es Salam projected to have population of 50 million around 2050-60 need for urbanization is imperative.

The 15 digital transformation point plant is shown by the KaribuTech AI team to help banks in Africa transform and adapt to the AI, Blockchain and Banking as Service boom

2.1 Can legacy insurers use digital transformation?

Legacy Banks in Africa are limited by cost of converting to new technologies, security breaches, API non-readiness as well. The following can help transform into the modern future bank

2.3 Promising lights in digital transformation in African insurance?

African banks can take advantage of key technological advances including

a. Rollout of fiber and 5G network

b. Introduction of Satellite communication like StarLink

c. Introduction of eSim technology to enable MVNO in banks

- d. Huge increase ein FinTechs especially in the Mobile Money space

2.4 Can legacy insurers use digital transformation?

Legacy insurers in Africa are limited by cost of converting to new technologies, security breaches, API non-readiness as well based on the following

2.5 Triggers of digital transformation ?

Digital transformation is triggered when bank goes some form of transformation like a

Merger,

Acquisition,

Regulatory changes,

regional expansion.

2.6 Steps in digital transformation in insurance?

Digital transformation in banking refers to integrating various fintech technologies to automate, optimize, and digitize processes in the banking industry.

3. SWOT Analysis In African Insurers

a) Do a digital capability assessment of current state using different measuring frameworks.

b) The assessment is on both business capabilities and technical capabilities

3.2 Opportunities: The opportunities include the ability of the banks to convert the unbanked using such tools like mobile money and USSD as well as mobile app penetration. The threat being the high cost of data accross the region.

3.3 What are the strengths and weaknesses

a) The assessment objectives include the need to transform the customer experience for the African bank in the rural area as well as in the urban areas. The strengths in Africa is the high mobile penetration and also its young population hence they can embrace digitization easily.

b) Improving literacy rates, high GDP and economy growth rates and high population growth rates gives Africa a competitive edge in being a banking market.

c) Insurers can benefit from the following in digitization

3.4. Insights: This dimension caters to realize how well an organization

utilizes business and customer information to measure their success metrics in various domains

4. Carry OUT ASSESSMENT OF WHATS There

a) Do a digital capability assessment of current state using different measuring frameworks.

b) The assessment is on both business capabilities and technical capabilities

c) AI, Blockchain, Automation, Low Code platforms and big data analytics drive the key needs of this digital bank

d) Changing customer needs, digital adoption, social media and customer personalisation needs also drive this bank of the future picture.

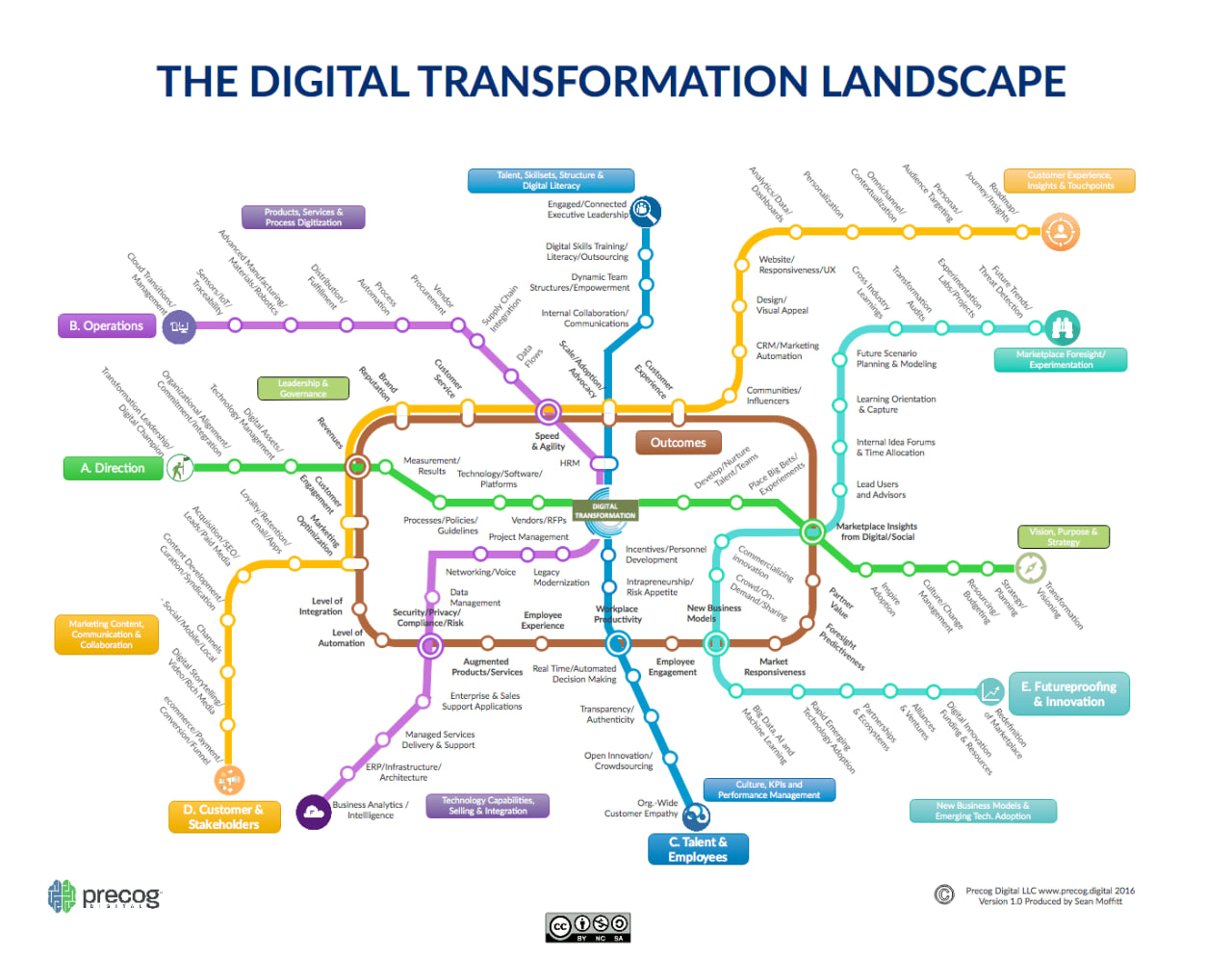

e) Measurement of current as is can use such frameworks like the Temenos Value Benchmark as shown in the diagram

Forrester’s Digital Business Maturity Model 4.0. has skeptics, adopters, collaborators and Differentiators ad levels of maturity. Key

4.1. Culture: caters to an

organization’s focus towards digital advancement and considers the need to empower employees

with digital technology and equip them with digital trainings.

4.2. Technology: This dimension adheres to the need for adoption of cutting edge and emerging technologies by the company.

4.3. Organization: This dimension caters to the steps taken by company to support governance, digital strategy, and execution.

4.4. Insights: This dimension caters to realize how well an organization

utilizes business and customer information to measure their success metrics in various domains

The following integration assessment model can also be used to check level of automation and business process maturity.

Other measurement maturity models that can be used include

4.5 Other measurement maturity models that can be used include:

1. McKinsey Digital Quotient: This model assesses an organization's digital transformation maturity in four stages: Beginner, Intermediate, Advanced, and Leading. The model focuses on four critical areas: Strategy, Culture, Organization, and Operations.

2. Capgemeni Digital Maturity Assessment model

3. ISACA®’s Capability Maturity Model Integration (CMMI®) model.

4. Gartner Digital Business Maturity Model: This model assesses an organization's digital transformation maturity in five stages: Stage 1: Analog, Stage 2: Digital Marketing, Stage 3: Digital Business, Stage 4: Digital Ecosystem, and Stage 5: Autonomous Business. The model focuses on five critical areas: Strategy, Leadership, People, Process, and Technology.

4. Deloitte Digital Transformation Maturity Model: assesses an organization's digital transformation maturity in five stages: Traditionalist, Fashionista, Follower, Digirati, and Digital Leader. The model focuses on three critical areas: Strategy, Talent, and Technology.

5. Map out what the Target Insurer needs to be

5.1 The new strategy governed by regulatory impediments, market competition, budget limits govern how the bank of the future needs to look like.

5.2 Changing customer needs, digital adoption, social media and customer personalization needs also drive this bank of the future picture.

5.3 AI, Blockchain, Automation, Low Code platforms and bigdata analytics drive the key needs of this digital bank

5. 4 Insurers can choose based on their strategy which model they want to get into

Whatfix")

5. Define BuSiness Architecture Capabilities

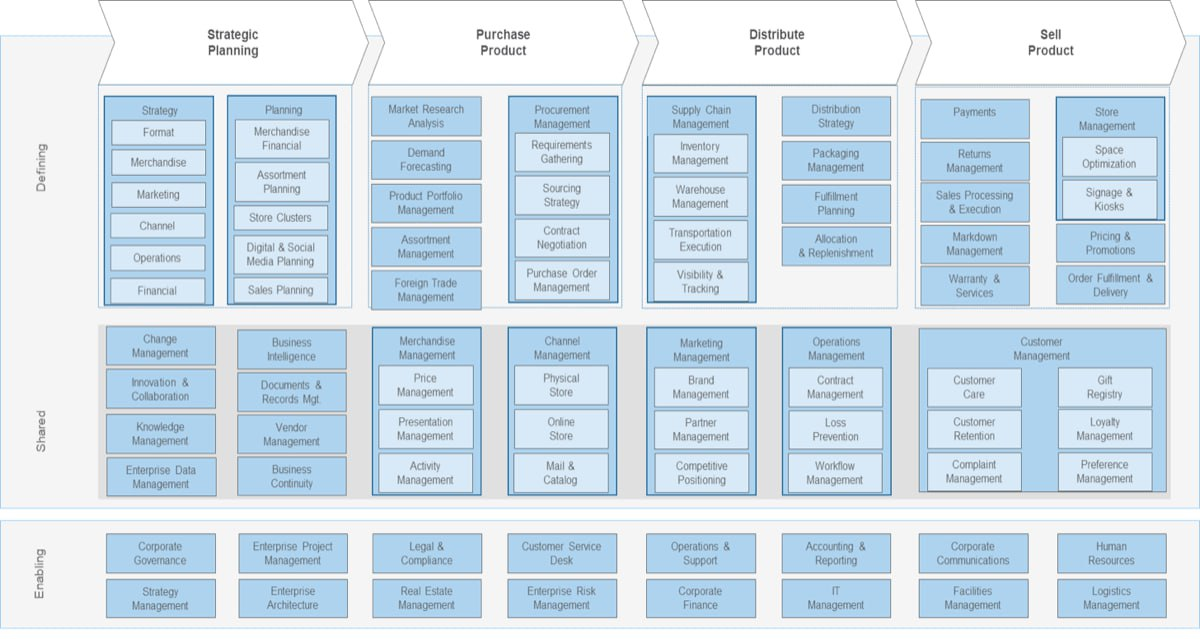

5.1 The business architecture will include defining of key value streams categorising the business entity of the bank. Key recommendations include adoption of TOM as an architecture framework.

5.2 Business centric capabilities should be the ones measured using a customer centric approach

The business architecture will include defining of key value streams categorising the business entity of the bank. Key recommendations include adoption of TOM as an architecture framework.

The business architecture will include defining of key value streams categorising the business entity of the bank. Key recomendations include adoption of TOM as an architecture framework.

5.6 Key steps that can be followed include the following

The timelines of the above steps depend on the insurance strategy of transformation and reason for transformation. Regulatory transformation timelines however can not be changed

5.7 Key stakeholders in the exercise include enterprise, solution and local business and IT teams as well as Fintech partners

5.8. These options for the mapping can be done in different approaches including the following:

5.9. Inclusion of fintechs and open insurance partners is critical and some of the partners that can be involved in the mapping of the business capabilities include the following.

6. Define the future capability and value streams stack

The business architecture will include defining of key value streams categorising the business entity of the insurer.

6.1 The business architecture will include defining of key value streams categorising the business entity of the insurance company. Key recomendations include adoption of TOM as an architecture framework.

6.2 The insurance business architecture will include defining of key value streams categorising the business entity of the insurance division. Modern banks incorporate banking and insurance in one.

6.3 The business architecture will include also consider other capabilities including regulatory changes, security as well as customer data. security and risk management

6.4 The business architecture will include defining of key value streams categorising the business entity of the insurer

7. Define the future technology stack

The Technology architecture will include defining of key value streams categorising the business entity of the bank. Key recommendations include adoption of TOM as an architecture framework.

7.1 Five components of the architecture is recommended

Other business capabilities taken into account that can be used include

7.2 Self service capabilities are key in the modern insurer

7.3 The architecture can be in the evolving , mature or optmised stage

The approach should always be following an omni-channel approach

7.4 Other components include the Core Insurance Architecture, the CRM Architecture, Data Architercture as well as Payment Architecture and other business units

8. Define the core insurance system strategy

The Core insurance Technology architecture will consider, cost, time to market, API readiness as part of its migration and transition into new ready core banking technologies.

")

8.2 Full replacement of the core with a new tech stack. Insurers often pursue this course of action when they urgently need to replace their core platforms because of obsolescence or regulatory imperatives. However, it can be risky.

It requires extensive data migration and the benefits are typically only realized when the final customer is migrated and the legacy systems are decommissioned.

8.3 Banks generally choose a traditional platform as the replacement, reflecting concerns that next-generation platforms are not yet fully proven or focused on a subset of products and features.

8.4 Legacy platforms inhibit performance:

Cost. Cost is more important than ever given low industry return on equity (ROE). Yet technical debt in legacy systems consumes large chunks of IT spend

Time to market. Being able to launch products quickly is a critical competitive differentiator in the current crowded marketplace.

Personalization. Customers increasingly expect a personalized experience. But insurers often store data in multiple product-aligned core systems, which inhibits catering to individual needs.

9. Adopt Cloud Computing

The insurer can adopt a mixed strategy with onprem for high risk solutions and regulatory monitored solutions, cloud on AWS, Azure and Alibaba for Platform Insurance,

1. Platform as a Service,

2. Software as a Service Solutions or

3. Other functions and also use third party solutions.

10. Adopt AI and IOT

10.1 The business architecture will include defining of key value streams categorising the business entity of the bank. Key recommendations include adoption of TOM as an architecture framework.

10.2 The Claims business architecture will include defining of key value streams categorising the insurance entity.

10.3 The AI components in insurance include use of

11. Adopt Platform Insurance

11. 2 Platform Insurance is a digital marketplace enables an insurer to sell other non insurance and create a marketplace using such tools like superapps as well as creating guarantees for service providers and link clients on the service platform.

Insurers can sell airtime, provide funeral services and other services like photography as well as provide towing services.

11. 2 Platform Insurance is a digital marketplace that is owned and maintained by an insurer or another third party and provides insurance and noninsurance services.

11.3 The insurer can adopt a mixed strategy with onprem for high risk solutions and regulatory monitored solutions, cloud on AWS, Azure and Alibaba for Platform Banking,

1. Platform as a Service,sell other services using mobile superapps and eCommerce mall capabilities

2. Software as a Service Banking Solutions or

3. Other functions and also use third party solutions.

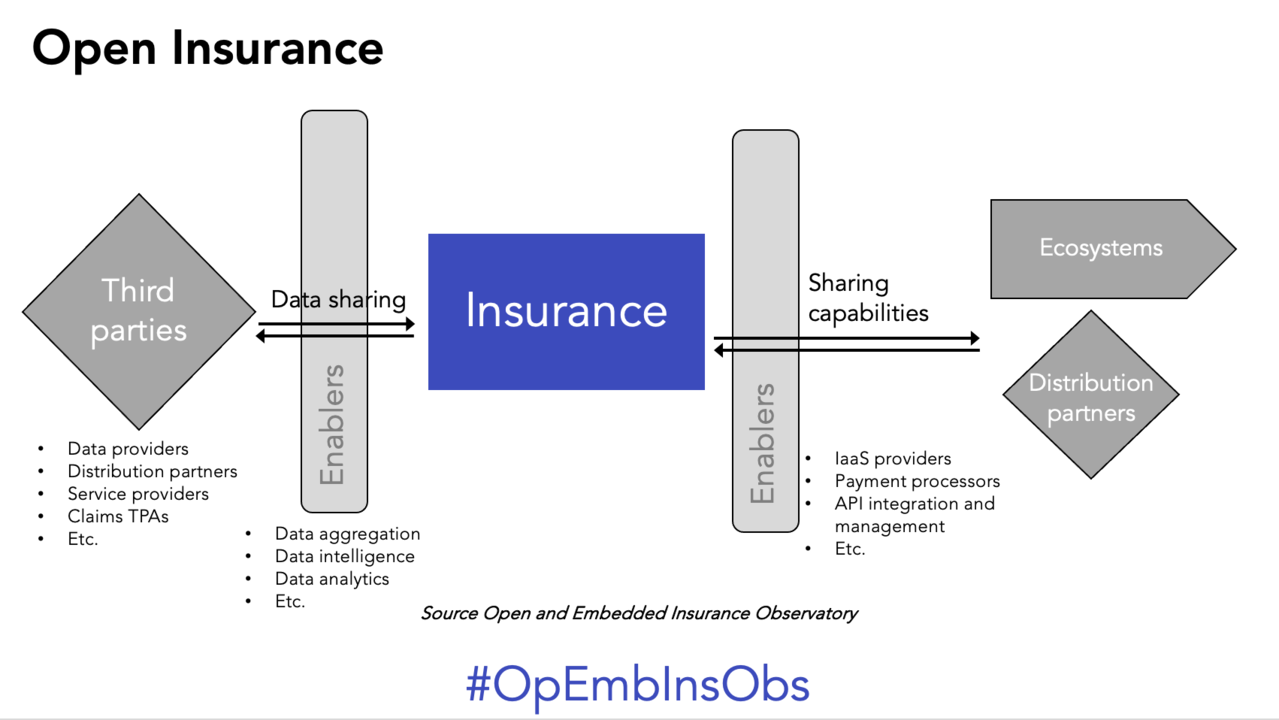

12. Adopt Open Insurance

12.1 With open insurance the digital insurer utilise best of the best strategy utilities in the market and also change whenever they need using APIs. Pay as you use is one major advantage

12.1 End user journeys can be defined to align with an open banking strategy

13. Adopt Insurance as a Service

With IaaS the insurers can adopt

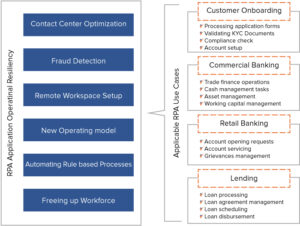

14. Adopt RPA, Low Code

With open banking the digital bank utilise best of the best strategy utilities in the market and also change whenever they need using APIs. Pay as you use is one major advantage

With low code platforms time to market of internal solutions are rapid

For commercial banking, customer onboarding, retail banking and lending, low code platforms can be used to do internal frontend capabilities which doesnt need exterior nice functions.

Example frameworks used in the banking space include the following

Workfusion

UIPath

Blueprism

15. Adopt Generative AI

With open banking the digital bank utilise best of the best strategy utilities in the market and also change whenever they need using APIs. Pay as you use is one major advantage

With low code platforms time to market of internal solutions are rapid

With open banking the digital bank utilise best of the best strategy utilities in the market and also change whenever they need using APIs. Pay as you use is one major advantage

16. Adopt A Data Centric Architecture

With open banking the digital bank utilise best of the best strategy utilities in the market and also change whenever they need using APIs. Pay as you use is one major advantage

With low code platforms time to market of internal solutions are rapid

Example tools that can be use on the cloud or on prem with licensing or open source are shown in the table below

Data forms a 3 pivot for a modern bank with cloud adoption and microservices applications

17. Adopt Process Automation as center pivot

- 17.1 Automation should be central to most of the bank processes including onboarding, mantanance , payments and other third party services like procurement. Model processes from major workflow houses like IBM, Oracle's templates can be used to kickstart the onboarding journey.

- 17.2 Automation also includes Process Mining which enables AI prediction of future events.

- Technologies like IBM BPM, Camunda, Pega, Oracle Fusion can be used

- BPM notations include using BPMN, BPEL and CMMN process modelling techniques and DMN and FEEL for rules capabilities

- 17.3 The following process shows a mortgage approval process the bank can adopt

- Automation also includes Process Mining which enables AI prediction of future events.

- Technologies like IBM BPM, Camunda, Pega, Oracle Fusion can be used

- BPM notations include using BPMN, BPEL and CMMN process modelling techniques and DMN and FEEL for rules capabilities

17.4 Digital Process that can adopt automation include

- New Business Onboarding for both personal and corporate

Payments Approval on delegation of duty

Customer Mantainance and Agents Processing

- Claims processing and reinsurance

18. Center of Excellence

18.1 Design Center of Excellence for staff to create long term strategy

a. saves multiple groups from continually “reinventing the wheel” by defining the same process again and again.

- b. The processes created by CoE are most likely more efficient than processes created on the fly by less qualified individuals.

19. Adopt SAFE Agile

9.1 Adopt SAFE Agile Methodology

Monitoring tools like AppDynamics and Prometheus and Grafana

Digital transformed banks are defined by modern security and risk and compliant frameworks

10.2 The AI Framework adoption includes data, risk monitoring, prevention and measurement.

Plan for next generation technologies in a span of a decade and beyond, Electrical Cars, Quantum Computing etc