OUR Banking Strategy with Ntantokazi

Banking with Automation

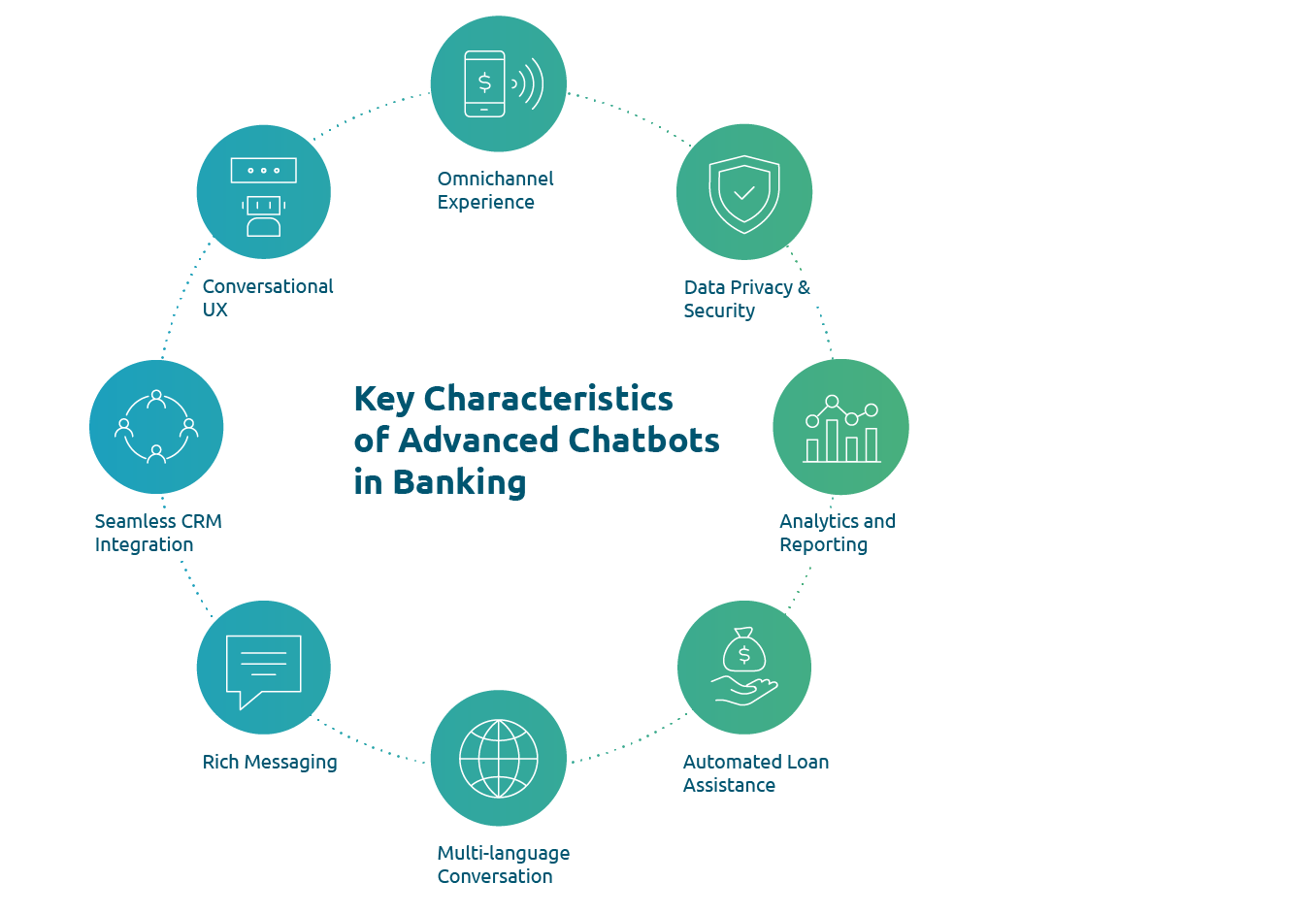

We automate key bank processes including retail , investment and wealth banking and these are key templates we have

OUR SERVICES

We work with change-oriented executives to help them make better decisions, convert those decisions to actions.

The rise of micro-financing has been rapid in first and third world countries. Some of the options include peer to peer and unsecured lending

The rise of micro-financing has been rapid in first and third world countries. Some of the options include peer to peer and unsecured lending. Micro lending solutions are high risk because of insufficient data on the customer’s credit history. Micro lenders and peer to peer lenders face high competition and high levels of defaulting since most the loans are unsecured.

Defaulting has been worsened by high costs of loan collections, delays in payroll deductions and global macroeconomic fluctuations. Some legislative rules increase the risk of defaulting on the personal loans. Loan collection methods are poor and slow as well. The use of a blanket credit scoring models for small scale lenders is not optimal for the risk and business they operate and this is exacerbated by having large unsecured loans portfolios.

With rising unemployment there is need to offer unsecured, or no collateral loans and small lenders need default lending predictors using machine learning. The ability to predict loan defaults can help loan providers in not only the loan application phase, but also for early intervention strategies to possibly prevent defaulting for peer to peer lenders. New machine learning algorithms like deep learning, XGBoost, LightGBM and CatBoost are used to classify peer to peer lending information.

The rise of micro-financing has been rapid in first and third world countries. Some of the options include peer to peer and unsecured lending

The rise of micro-financing has been rapid in first and third world countries. Some of the options include peer to peer and unsecured lending. Micro lending solutions are high risk because of insufficient data on the customer’s credit history. Micro lenders and peer to peer lenders face high competition and high levels of defaulting since most the loans are unsecured.

Defaulting has been worsened by high costs of loan collections, delays in payroll deductions and global macroeconomic fluctuations. Some legislative rules increase the risk of defaulting on the personal loans. Loan collection methods are poor and slow as well. The use of a blanket credit scoring models for small scale lenders is not optimal for the risk and business they operate and this is exacerbated by having large unsecured loans portfolios.

With rising unemployment there is need to offer unsecured, or no collateral loans and small lenders need default lending predictors using machine learning. The ability to predict loan defaults can help loan providers in not only the loan application phase, but also for early intervention strategies to possibly prevent defaulting for peer to peer lenders. New machine learning algorithms like deep learning, XGBoost, LightGBM and CatBoost are used to classify peer to peer lending information.

The rise of micro-financing has been rapid in first and third world countries. Some of the options include peer to peer and unsecured lending

The rise of micro-financing has been rapid in first and third world countries. Some of the options include peer to peer and unsecured lending. Micro lending solutions are high risk because of insufficient data on the customer’s credit history. Micro lenders and peer to peer lenders face high competition and high levels of defaulting since most the loans are unsecured.

Defaulting has been worsened by high costs of loan collections, delays in payroll deductions and global macroeconomic fluctuations. Some legislative rules increase the risk of defaulting on the personal loans. Loan collection methods are poor and slow as well. The use of a blanket credit scoring models for small scale lenders is not optimal for the risk and business they operate and this is exacerbated by having large unsecured loans portfolios.

Defaulting has been worsened by high costs of loan collections, delays in payroll deductions and global macroeconomic fluctuations. Some legislative rules increase the risk of defaulting on the personal loans. Loan collection methods are poor and slow as well. The use of a blanket credit scoring models for small scale lenders is not optimal for the risk and business they operate and this is exacerbated by having large unsecured loans portfolios.

With rising unemployment there is need to offer unsecured, or no collateral loans and small lenders need default lending predictors using machine learning. The ability to predict loan defaults can help loan providers in not only the loan application phase, but also for early intervention strategies to possibly prevent defaulting for peer to peer lenders. New machine learning algorithms like deep learning, XGBoost, LightGBM and CatBoost are used to classify peer to peer lending information.

Defaulting has been worsened by high costs of loan collections, delays in payroll deductions and global macroeconomic fluctuations. Some legislative rules increase the risk of defaulting on the personal loans. Loan collection methods are poor and slow as well. The use of a blanket credit scoring models for small scale lenders is not optimal for the risk and business they operate and this is exacerbated by having large unsecured loans portfolios.

Defaulting has been worsened by high costs of loan collections, delays in payroll deductions and global macroeconomic fluctuations. Some legislative rules increase the risk of defaulting on the personal loans. Loan collection methods are poor and slow as well. The use of a blanket credit scoring models for small scale lenders is not optimal for the risk and business they operate and this is exacerbated by having large unsecured loans portfolios.

CHOOSE YOUR PLAN

You’ve Got All Reasons to

Move Your Team to Blufountain Banking Right Now

Our management consulting services focus on our clients’ most critical issues and opportunities: strategy, marketing, organization, operations, technology, transformation, digital.

BASIC PLAN

$

/Per Month

ULTRA PLAN

$

/Per Month

PREMIUM PLAN

$

/Per Month

OUR SKILLS

The Team of Innovators

Our uniquely collaborative and passionate people work alongside our clients every step of the way—caring more, telling it like it is—to anticipate and overcome all the barriers to change.